Detroit has been hit particularly hard due to the already struggling automotive industry, so the recession just brought about more reasons of layoffs. The last four unemployment numbers have been very positive however.

Keep dancin'

Steven J.

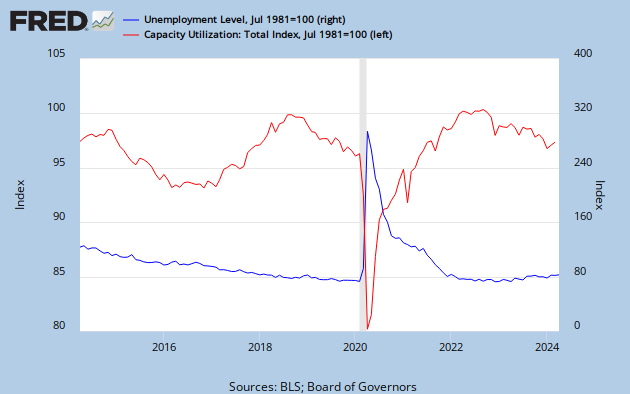

"That is, in past recessions an upturn in capacity utilization was matched by an upturn in employment, there was no delay in the relationship, but in recent recessions there has been about a half year delay before unemployment reacts to changes in capacity utilization (or perhaps even a bit longer)."We can definitely see this delay in the 2001 recession. Notice how capacity utilization turns up and unemployment is initially very slow to drop. The argument is being made that we are going to see the same thing this time around, where capacity utilization rates improve but unemployment won't drop for at least half a year.

"Usually housing starts and residential construction employment lead the economy out of a recession, but not this time because of the huge overhang of existing housing units. After rebounding a little in early '09, housing starts have mostly moved sideways"

"the federal stimulus (of which 75 percent has been spent), near-zero interest rates (which can’t continue much longer without igniting speculative bubbles), and replacements (consumers have had to replace worn-out cars and appliances, and businesses had to replace worn-down inventories)."Another bad sign is that some of the insiders like the super-rich believe that a double-dip will indeed occur. Robert Frank of WSJ's Wealth Report, wrote that the super rich were buying gold again and how troubling that is. For additional support he points to a survey of the rich and super rich which found that 25% of those with a net worth of $15 million or more believed the global economy will deteriorate in the next five years, compared with an average of 17% of respondents with $1.5 million or more. His theory (and i tend to agree with him on all three points) is that:

"First, the wealthy have better information than most Americans, and that information suggests more bad news to come.Second, the wealthy have more to lose (in pure dollar terms) than the nonwealthy. The risks of losing a fortune right now appear greater than the potential for building a fortune.

Third (and related to the second theory) the wealthy are making conservative bets with their money, avoiding bold trades and preferring to sit on cash. People who hang on their cash to preserve their fortunes are by nature going to be more cautious about the broader economy."

It will be interesting to see if all these rumors will become a self-fulfilling process as the economy's state is all of a sudden highly questionable. Macro Man is skeptical of the markets and economies ability to recover because the negatives seem to be overwhelmingly outweighing any positives, for example pointing to the recovery in manufacturing and how it's unlikely to be the miracle we're looking for. Macro Man is worried about all the problems in Europe becoming even worse as they brace themselves for epic disaster:

"In spite of the authorities the world over seemingly having thrown everything, including the kitchen sink at the problem, the market seems to have gone back to square one in the past couple of days. The panic in the EUR periphery not only continues unabated, but is now spreading to “soft-core” countries (Austria, Belgium, Finland) and France (welcome to the Club Med, Mr. Sarkozy)."

Initial unemployment insurance claims have been steadily falling since its peak in early 2009, but has seemed to level off around 460,000 which indicates that the economy is still weak and in danger of slipping back into contraction (possibly a double dip). A general rule of thumb is that when first-time claims stand above 400,000 for several weeks the economy may be in danger of slipping into a recession. A number below 400,000 suggests a recovery in underway and companies are laying off fewer workers.

Initial unemployment insurance claims have been steadily falling since its peak in early 2009, but has seemed to level off around 460,000 which indicates that the economy is still weak and in danger of slipping back into contraction (possibly a double dip). A general rule of thumb is that when first-time claims stand above 400,000 for several weeks the economy may be in danger of slipping into a recession. A number below 400,000 suggests a recovery in underway and companies are laying off fewer workers. The above graph shows the two recessions of the early 1980's where initial unemployment claims originally leveled off slightly above 400,000 before the economy slipped into another contraction. I have a feeling that maybe the same thing will happen in the most recent scenario given that the economy is still in a very fragile state.

The above graph shows the two recessions of the early 1980's where initial unemployment claims originally leveled off slightly above 400,000 before the economy slipped into another contraction. I have a feeling that maybe the same thing will happen in the most recent scenario given that the economy is still in a very fragile state.