Okay so here is what has been happening:

The yield curve has been going through a mad flattening- indicating that investors are "flying to safety" and that a recession may be looming around the corner. Why has it been flattening? Well, a string of bad news. For one, GDP numbers came out today and only indicated a 1.3% expansion. Considering the revisions in these numbers have been downward of late- this is not good news. GDP has been expanding but at a slowing rate signaling a possible peak around the corner.

Furthermore, Congress still has yet to come to an agreement with Tea Party-ers being the party poopers by acting completely unwilling to budge with Obama and now John Boehner. The situation does not look pretty. In fact, its unbearable to witness.

Additionally, consumer sentiment readings came out today at 63.7 which is consistent with recessionary levels.

The Contradiction:

SO we have been seeing people purchase treasuries instead of dumping them, like i had previously anticipated. Was i wrong? Clearly i was. What did i not consider? Treasuries are the most liquid and safe security on earth and quite frankly there is no close substitute. Gold is not a substitute even though there has been quite the flight to it. Why? Its not very liquid and therefore don't depend on it as much for collateral.

Whatever the case may be we are seeing something extraordinary and totally expected:

TOTAL MASS CONFUSION

Please people! Keep Dancin'

Steven J.

Showing posts with label Debt. Show all posts

Showing posts with label Debt. Show all posts

Friday, July 29, 2011

Monday, July 18, 2011

The Road to Default: Puppy Power!

Although Congress can technically dilly dally until August 2nd to come up with an agreement and raise the debt ceiling- markets have anticipated the inevitable. They haven't sat back and decided to wait till August 2nd to panic- they are already in "oh shit" mode. On this note a recent CNBC interview with David Murrin suggests that I am not alone:

A U.S. default isn't a matter of "if" but "when," David Murrin, chief investment officer at Emergent Asset Management, told CNBC. "It's inevitable that the U.S. will default—it's essentially an empire which is overextended and in decline—and that its financial system will go with it," he said.

Uncertainty about what Congress is going to do has forced investors to assume that Congress will screw it up. Steven Hess of Moody's explains this as "event risk" and today suggested that the United States eliminate its statutory limit on government debt to reduce uncertainty among bond holders.

"The current wide divisions between the House of Representatives and the Obama administration over the debt limit creates a high level of uncertainty and causes us to raise our assessment of event risk," Hess said.

This additional "event risk" is just one additional factor that encourages ratings agencies to downgrade the United States AAA credit rating.

Unsurprisingly enough, we have already seen the Dow Jones fall 1.1% today. Surprisingly, Treasury yields have remained unscathed. Furthermore, there has been an increasing capital "flight to safety" as Gold hit a new high today. Investors are just chillin' and waiting for the news that will trigger the dumping of Treasuries. I have a feeling that this is the present situation because investors aren't buying Treasuries, but they're also not selling them, instead we see the flight to safer assets from stocks directly to Gold and Silver. I will be following the news as it unfolds with both ears perked ready to hear the verdict. This is the casey anthony trial for the financial markets.

Who is going to save the world? Will it be a bunch of cute puppies fighting crime and licking the face of someone in a state of post traumatic stress? Unfortunately, i don't think any amount of cute puppies will be able to cause congress to agree on a sustainable and credible debt deal in the near future. That is why I ask who is going to save to world? If not cute puppies- then who?

Timmy G of the U.S. treasury? Benny B of the Fed? Or will our nation just rise up like Chris Angel and produce a resolution out of thin air?

Keep shufflin'

Steven J.

Saturday, July 16, 2011

The Road to Default: Deep DooDoo

Okay so what is the situation at hand? Well the inevitable default of the United States of course. The U.S. will default regardless of whether Congress raises the debt ceiling. You may be thinking the following: But how can he say such a thing? Is there anything we can do to stop it? There is no way that can be true!

Let me convince you that we're in deep shit.

First: Look at Italy. Until this past week they were considered a safe haven for bondholders. Then their eurobonds jumped up to 6% because investors got spooked. Nothing happened that would suggest that they are in fiscal demise. There is no real political instability or real danger of default and Italy's banks are relatively well capitalized with mostly retail deposits.

The U.S. on the other hand has had petitions being signed by influential economists and businessmen urging congress to raise the debt ceiling to come to an agreement. We also have had default and debt recently come to the center stage and center of attention. In financial markets, anything that even gets a little press ends up being way worse than initially anticipated. For examples of this just look at the subprime mortgage market and how early warning signs were easily dismissed.

In Charles Poor Kindleberger's famous book on the history of financial crisis, one of the most tell tale signs of a major breakdown looming is when a central banker or someone important gives an early warning. The example we can draw from is in 1996 when then chairman Alan Greenspan warned of "irrational exuberance" to describe the tech bubble. In terms of prescience we have seen numerous warnings from Benny Bernanke about our debt buildup.

No matter what happens the U.S. will default. Cautious investors should get the picture if they haven't already that now is the time to cash out and see what happens. I could be wrong- but the turbulence that will ensue regardless as Congress fights over what to do will not be worth the hassle. My game plan would be to buy back in when yields spike and they could spike by quite a lot. S&P was even recently taking about downgrading U.S. treasuries to AA status regardless of a debt ceiling negotiation. Yields will spike. I promise you and now you have to promise me to keep dancin'

Steven J.

Let me convince you that we're in deep shit.

First: Look at Italy. Until this past week they were considered a safe haven for bondholders. Then their eurobonds jumped up to 6% because investors got spooked. Nothing happened that would suggest that they are in fiscal demise. There is no real political instability or real danger of default and Italy's banks are relatively well capitalized with mostly retail deposits.

The U.S. on the other hand has had petitions being signed by influential economists and businessmen urging congress to raise the debt ceiling to come to an agreement. We also have had default and debt recently come to the center stage and center of attention. In financial markets, anything that even gets a little press ends up being way worse than initially anticipated. For examples of this just look at the subprime mortgage market and how early warning signs were easily dismissed.

In Charles Poor Kindleberger's famous book on the history of financial crisis, one of the most tell tale signs of a major breakdown looming is when a central banker or someone important gives an early warning. The example we can draw from is in 1996 when then chairman Alan Greenspan warned of "irrational exuberance" to describe the tech bubble. In terms of prescience we have seen numerous warnings from Benny Bernanke about our debt buildup.

No matter what happens the U.S. will default. Cautious investors should get the picture if they haven't already that now is the time to cash out and see what happens. I could be wrong- but the turbulence that will ensue regardless as Congress fights over what to do will not be worth the hassle. My game plan would be to buy back in when yields spike and they could spike by quite a lot. S&P was even recently taking about downgrading U.S. treasuries to AA status regardless of a debt ceiling negotiation. Yields will spike. I promise you and now you have to promise me to keep dancin'

Steven J.

Monday, July 11, 2011

The Road to Default: Debt Ratio Comparison's With Previous Episodes

In 2009, Carmen M. Reinhart and Kenneth S. Rogoff wrote a book titled ,"This Time Is Different" about debt and financial crisis. One of their charts will provide a benchmark for us in our analysis. This chart can be found on page 121 of the book and shows the ratios of public debt to revenue immediately preceding an external default. For Africa the external debt/ revenue ratio was 1, Asia it was 1.5, in Europe it's 1.6ish and for Latin America its closer to 3. As the following chart explains our current ratio in the United States is around 1.7ish which is higher than in Africa, Asia and Europe at the time of an external default.

Additionally the chart in "This Time Is Different" also compares the ratios of total debt to revenue at the time of the default. For Africa is was 2.6ish, in Asian countries the ratio lies around 4, in Europe it hovers around 3.75 and for Latin America around 4.6ish. As the following chart shows, we are considerably past this doomed territory with a public debt-to- revenue ratio of around 5.61 and climbing. The following graph I did in R because it just seemed easier.

So the lesson's learned today are that by history's benchmarks the U.S. is way past the point of no return and all we can do is hold on for the ride of a lifetime or prepare for the Federal Government to cut spending by a large enough amount that real GDP growth will most likely slow to a stall. It's a lose-lose situation. Prepare for pain, but keep dancin',

Steven J.

Sunday, July 10, 2011

The Road to Default: Who's getting the most screwed?

Let's take a look at who gets the most screwed (who loses the most money) when bond prices collapse and the United States defaults.

Well until recently only about 55% of treasury's were held domestically. The rest was externally held by places like Japan and China. Now something like 67% is held domestically, which means when shit hits the fan, the majority of the burden will be on the U.S., however that isn't even the 1/3rd's of it. Considering that 33% is held externally, we could be in some trouble especially if China keeps looking to the Euro to diversify its investments. We could see even further downward pressure on treasuries leading to an even higher interest rate burden. I know I will keep shuffling through the default, but will John Boehner? The dude who has refused to make a deal with the Democrats despite pleading from the Economist Magazine, President Obama, Chairman Benny B and Financial Markets everywhere. Good luck America and keep dancin,

Well until recently only about 55% of treasury's were held domestically. The rest was externally held by places like Japan and China. Now something like 67% is held domestically, which means when shit hits the fan, the majority of the burden will be on the U.S., however that isn't even the 1/3rd's of it. Considering that 33% is held externally, we could be in some trouble especially if China keeps looking to the Euro to diversify its investments. We could see even further downward pressure on treasuries leading to an even higher interest rate burden. I know I will keep shuffling through the default, but will John Boehner? The dude who has refused to make a deal with the Democrats despite pleading from the Economist Magazine, President Obama, Chairman Benny B and Financial Markets everywhere. Good luck America and keep dancin,

Steven J.

Steven J.

Saturday, July 9, 2011

The Road to Default: We Crumble Like A Cookie

keep dancin'

Steven J.

Friday, July 8, 2011

The Road to Default: Let's Look at the Damage with a Rant.

The following graph shows Real GDP as a percentage of the Gross Federal Debt. FRED is the resource I frequently use for United States financial data and it serves us well here.

The following graph shows Real GDP as a percentage of the Gross Federal Debt. FRED is the resource I frequently use for United States financial data and it serves us well here. What is Gross Federal Debt? Well, its total government debt outstanding- including all the various agencies.

Why do we compare real GDP with it? We want to hypothetically see that even if we have a 100% tax rate for one year and kill every business we still couldn't eliminate all of our Government debt!

Notice that we are at above 100%! Default is inevitable! Raising taxes (aka revenue) is frivolous at this point, the only way to bring this unsustainable rise in debt down it to deleverage by way of default. This is the only way because our politicians are resolved to not do anything and to see what happens. Their lives are more important than ours and that is why they may refuse to engage in political blasphemy (cutting medicare, down sizing social security payments, ending unemployment benefits).

The Republicans & FOX NEWS will blame the default on President Obama and John Stewart, no matter how ridiculous and untrue that may be.

The Democrats will blame it on the Republicans refusal to come to a deal sooner. In the end both will be severely discredited. I will blame it on our political system. It dooms us. How can anyone make a politically unpopular decision when they are worried about getting re-elected? They can't and they won't most likely. Our country is in trouble and it's not because Casey Anthony was found not guilty, that we don't allow drilling in the gulf, or that we have millions of illegals pouring over the border. It's not the small and meaningless stuff. It's the structure of our broken system, the stubbornness of our elderly, and most importantly it's a failure to be truthful and do what's right.

"The nation's long-term fiscal imbalances did not emerge overnight. To a significant extent, they are the result of an aging population and fast-rising health-care costs, both of which have been predicted for decades. The Congressional Budget Office projects that net federal outlays for health-care entitlements--which were 5 percent of GDP in 2010--could rise to more than 8 percent of GDP by 2030. Even though projected fiscal imbalances associated with the Social Security system are smaller than those for federal health programs, they are still significant. Although we have been warned about such developments for many years, the difference is that today those projections are becoming reality."

We have a severely flawed tax system that would cause no uprise if only it was consumption based, a financial system that gets drunk every year off new financial innovations and lack of regulation, and media that "tells" the truth- even when they lie. I'm not a religious man, but God help us!

Keep Dancin'

Steven J.

Tuesday, August 10, 2010

From Private to Public: A Transfer of Debt

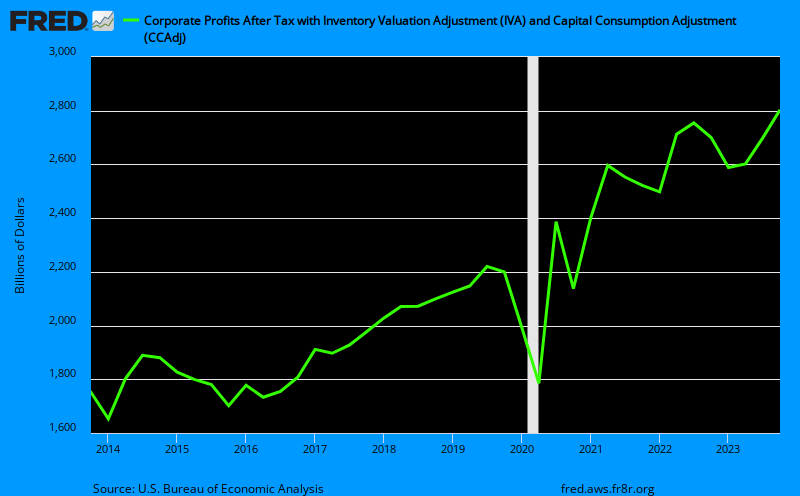

Corporate profits go up in recessions as mass layoffs lower operating costs and reduce corporate debt levels. Furthermore, the government takes the hit through unemployment insurance benefits, bailouts and lower income and sales tax receipts.

Corporate profits are going up, this is the result of massive layoffs and cutbacks, which also has raised workers productivity levels:

Debt levels are falling as more people are defaulting and are finding themselves in the 1-in-4 poor FICO credit score of 600 or less:

The financial obligations (total consumer and auto loans plus total consumer debt and mortgage debt) as a percent of disposable personal income (or income after taxes) has shown a semi-significant decline:

Were is all this debt being transfered to? The Federal Governments balance sheet: unemployment insurance claims first skyrocketing and now remaining steady:

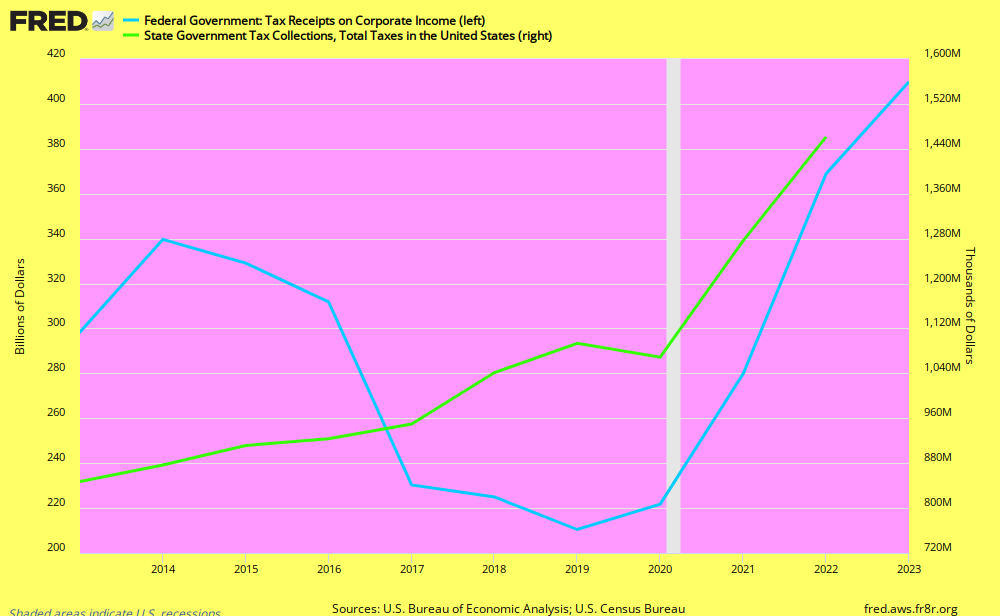

Government bailouts also lowered private debt levels and the biggest hit comes from decreased revenue from federal taxes on corporate profits and state income taxes:

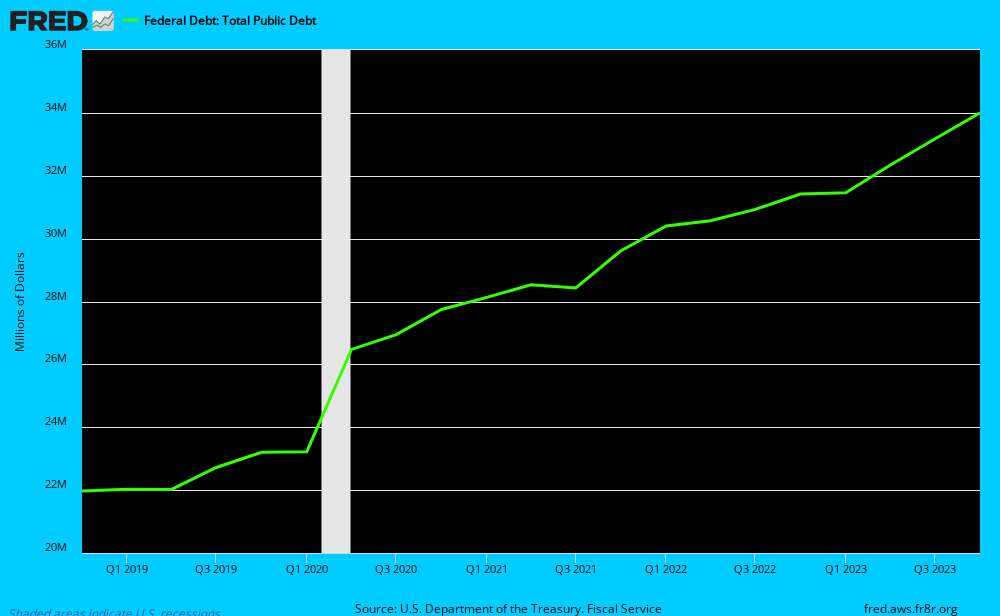

But it all adds up to a skyrocketing increase in the public debt:

There has been an effective transfer from the private sector to the public sector.

Corporate profits are going up, this is the result of massive layoffs and cutbacks, which also has raised workers productivity levels:

Debt levels are falling as more people are defaulting and are finding themselves in the 1-in-4 poor FICO credit score of 600 or less:

The financial obligations (total consumer and auto loans plus total consumer debt and mortgage debt) as a percent of disposable personal income (or income after taxes) has shown a semi-significant decline:

Were is all this debt being transfered to? The Federal Governments balance sheet: unemployment insurance claims first skyrocketing and now remaining steady:

Government bailouts also lowered private debt levels and the biggest hit comes from decreased revenue from federal taxes on corporate profits and state income taxes:

But it all adds up to a skyrocketing increase in the public debt:

There has been an effective transfer from the private sector to the public sector.

Thursday, July 15, 2010

What does a debt deflation entail and are we headed for one?

The process of debt deflation goes a little something like this:

Unemployment increases this leads to a sudden drop in income and more people filing for unemployment insurance. Suddenly people feel poorer and both home spending and consumer spending decline. Producer Prices then fall because business are cutting back on inventories. Furthermore, lower import prices also puts downward pressure on consumer and producer prices. Last but not least home prices continue to fall. Consumer prices then decrease due to lower input costs (via producer price index declines and import price declines) - this lower price level causes the real value of the debt burden to increase. This increased financial strain will lead to the next round of defaults and further reduction in consumer spending. This leads to more unemployment and even worse some unemployed 27 weeks or longer are no longer eligible for unemployment insurance. This leads to a further decline in incomes leading to more cash strapped households on the brink of desperation and another round of defaults as some (newly unemployed or uninsured laborers) are unable to make their debt payments.

Debt Deflation in the Economy:

Recession Hits ----> Unemployment (Increases) + Unemployment Insurance (Increases) ---> Income (Falls) -----> Spending (Falls)([Consumer Spending (Falls) + Home Spending (Falls)] )------> Price Level (Falls) ([ Producer Prices (Fall) + Import and Export prices (Fall) + Home Prices (Fall)]-----> Consumer Prices (Fall)] ) --> Real Debt Burden (Increases) --> Defaults (Increase) ---> Consumer Spending (Falls) --> Further Unemployment (Increases) + Unemployment Insurance (Fall)]---> Income (Falls) ----> Defaults (Increase) + Consumer Spending (Falls)---> and on and on

Lets look at the most recent evidence:

Unemployment has increased and those receiving unemployment insurance has decreased:

This is surely to have some more effects on the already depressed consumer and home spending:

The Producer Price Index has declined as of late to reflect the sharp cut back in production from businesses reaction to the lamesauce consumer demand:

Import prices have fallen recently:

Home spending and home prices continue to be trending downward:

Price deflation leads to an increased real debt burden and as we have seen defaults continue to be on the rise. As we have just seen some data suggest that this may be occurring and the fact that severe financial crisis do sometimes lead to debt deflation leaves me very worried. We would be experiencing a full-blown debt deflation right now if it wasn't for two things: sticky wages and unemployment insurance. The inflexible nature of wages allows those who do have jobs to keep spending. This - in addition to unemployment benefits - has prevented the severity of the crises from reaching the debt deflation stage. The governments ballooning debt has not been the work of bailouts but of unemployment insurance payments. This has represented a massive transfer of debt from the private to the public sector and the extension of these benefits have proved undeniably important for keeping our economy afloat.

Unemployment increases this leads to a sudden drop in income and more people filing for unemployment insurance. Suddenly people feel poorer and both home spending and consumer spending decline. Producer Prices then fall because business are cutting back on inventories. Furthermore, lower import prices also puts downward pressure on consumer and producer prices. Last but not least home prices continue to fall. Consumer prices then decrease due to lower input costs (via producer price index declines and import price declines) - this lower price level causes the real value of the debt burden to increase. This increased financial strain will lead to the next round of defaults and further reduction in consumer spending. This leads to more unemployment and even worse some unemployed 27 weeks or longer are no longer eligible for unemployment insurance. This leads to a further decline in incomes leading to more cash strapped households on the brink of desperation and another round of defaults as some (newly unemployed or uninsured laborers) are unable to make their debt payments.

Debt Deflation in the Economy:

Recession Hits ----> Unemployment (Increases) + Unemployment Insurance (Increases) ---> Income (Falls) -----> Spending (Falls)([Consumer Spending (Falls) + Home Spending (Falls)] )------> Price Level (Falls) ([ Producer Prices (Fall) + Import and Export prices (Fall) + Home Prices (Fall)]-----> Consumer Prices (Fall)] ) --> Real Debt Burden (Increases) --> Defaults (Increase) ---> Consumer Spending (Falls) --> Further Unemployment (Increases) + Unemployment Insurance (Fall)]---> Income (Falls) ----> Defaults (Increase) + Consumer Spending (Falls)---> and on and on

Lets look at the most recent evidence:

Unemployment has increased and those receiving unemployment insurance has decreased:

This is surely to have some more effects on the already depressed consumer and home spending:

The Producer Price Index has declined as of late to reflect the sharp cut back in production from businesses reaction to the lamesauce consumer demand:

Import prices have fallen recently:

Home spending and home prices continue to be trending downward:

Price deflation leads to an increased real debt burden and as we have seen defaults continue to be on the rise. As we have just seen some data suggest that this may be occurring and the fact that severe financial crisis do sometimes lead to debt deflation leaves me very worried. We would be experiencing a full-blown debt deflation right now if it wasn't for two things: sticky wages and unemployment insurance. The inflexible nature of wages allows those who do have jobs to keep spending. This - in addition to unemployment benefits - has prevented the severity of the crises from reaching the debt deflation stage. The governments ballooning debt has not been the work of bailouts but of unemployment insurance payments. This has represented a massive transfer of debt from the private to the public sector and the extension of these benefits have proved undeniably important for keeping our economy afloat.

Saturday, May 29, 2010

For the opposite view...

After writing the previous post on why budget deficits are a negative thing for the economy I stumbled upon an article that justified them. The Levy Economics Institute of Bard College recently released a Public Policy Brief on why we should stop worrying about U.S. Government deficits. The authors Yeva Nersisyan and L. Randall Wray point out that a budget deficit is just a transfer from the government to the private sector and that surpluses are the exact opposite net transfers from the private to government sector.

Furthermore, they dispute the often heard claim that deficit spending today burdens our grandchildren:

Furthermore, they dispute the often heard claim that deficit spending today burdens our grandchildren:

"in reality we leave them with government bonds that represent net financial assets and wealth. If the decision is made to raise taxes and retire the bonds in, say, 2050, the extra taxes are matched by payments made directly to bondholders in 2050”

Today's deficit leads to debt that must be retired later, and future tax increases that are supposed to service tomorrow's debt represent a redistribution from taxpayers to bondholders.

A government deficit is a transfer of income from the government to the private sector in the form of non-government income.

"A government deficit generates a net injection of disposable income into the private sector that increases saving and wealth, which can be held either in the form of government liabilities (cash or Treasuries) or noninterest-earning bank liabilities (bank deposits). If the nonbank public prefers bank deposits, then banks will hold an equivalent quantity of reserves, cash, and Treasuries (government IOUs), distributed according to bank preferences."

"A government budget surplus has exactly the opposite effect on private sector income and wealth: it’s a net leakage of disposable income from the nongovernment sector that reduces net saving and wealth by the same amount. When the government takes more from the public in taxes than it gives in spending, it

In defense of Obama's stimulus:

"These automatic stabilizers, not the bailouts or stimulus package, are the reason why the U.S. economy has not been in a free fall comparable to that of the Great Depression. When the economy slowed, the budget automatically went into a deficit, placing a floor under aggregate demand."

After reading this article, one highly theoretical argument that I can make is that if the United States was forced to monetize part of the debt it could raise interest on reserves to soak up any additional liquidity created in the system. This would represent a massive transfer of Government debt from the Treasury to the Fed in the form of excess reserves. The excess reserves could then be manipulated with the appropriate raising and lowering of the interest paid on reserves relative to the federal funds rate. This is quite an exciting premise that represents an internal transfer of funds by the U.S. Government that would keep inflation expectations stable while also calming the fears of deficit hawks.

Tuesday, May 25, 2010

Welcome to X.U. Economics/ Dangerous Defict

Hello y'all and welcome to the Xavier econ blog. This blog will be maintained by X.U. economics faculty and students, and will provide information on a variety of interesting topics in economics. Unfortunately for the world right now, one of the most fascinating yet dangerously risky current events just happens to be a global debt crises.

The world is on the verge of a global disaster. Just last week we saw Germany ban naked short selling, a sign that things are clearly only getting worse.

Before that investors around the world started closely watching the Greeks and their fiscal dilemma. That is also when I started watching. Greece was the first sign of a much deeper rooted issue. Greece was just the most over-leveraged of the euro-zone economies, and it revealed that countries similar to it would be endangered as well. If we look with our binoculars we can see that across the pond the whole euro-zone is panicking right now, and as they should be. Excessive budget deficits tend to erode confidence in the government. Whether in the United States or Greece the same principle holds regardless of economic status.

Confidence is very important to financial stability because everything is based off of future profits and cash flows. If confidence in the United States ability to pay back its debts and pay off its treasury notes erodes then we have a problem.

If the United States doesn't bring down its deficit:

A. The ratings agencies will see that debt/gdp ratio is outrageous, and will notice that the deficit is ballooning due to:

1. Lack of foreign demand for domestic goods which leads to decreased tax revenue

2. Rising interest rates since the Fed will have to raise the federal funds rate eventually

3. Reduced government cash flows due to a diminishing tax base with the high unemployment

4. Increased health care costs

5. Increased automatic stabilizers like transfer payments

B. The ratings agencies will then decide to downgrade U.S. Government debt which will lead to:

1. An increased budget deficit

2. Much higher interest rates

3. A massive sell off by all the major holders of U.S. Government debt, ( Many pension and insurance companies have it built into their computers to automatically sell bonds that are not AAA rated)

4. A further downgrade of U.S. debt

5. A massive sell off by China

For those of you who are still skeptical (most of you will be) read this speech by our Chairman of the Federal Reserve, it should help put some things in perspective. One thing to keep in mind is that when the Central Bank Chairman warns about fiscal sustainability it is usually a sign of too little will be done and whatever is done will be much too late in the game to make a difference.

As Ben puts it,

The world is on the verge of a global disaster. Just last week we saw Germany ban naked short selling, a sign that things are clearly only getting worse.

Before that investors around the world started closely watching the Greeks and their fiscal dilemma. That is also when I started watching. Greece was the first sign of a much deeper rooted issue. Greece was just the most over-leveraged of the euro-zone economies, and it revealed that countries similar to it would be endangered as well. If we look with our binoculars we can see that across the pond the whole euro-zone is panicking right now, and as they should be. Excessive budget deficits tend to erode confidence in the government. Whether in the United States or Greece the same principle holds regardless of economic status.

Confidence is very important to financial stability because everything is based off of future profits and cash flows. If confidence in the United States ability to pay back its debts and pay off its treasury notes erodes then we have a problem.

If the United States doesn't bring down its deficit:

A. The ratings agencies will see that debt/gdp ratio is outrageous, and will notice that the deficit is ballooning due to:

1. Lack of foreign demand for domestic goods which leads to decreased tax revenue

2. Rising interest rates since the Fed will have to raise the federal funds rate eventually

3. Reduced government cash flows due to a diminishing tax base with the high unemployment

4. Increased health care costs

5. Increased automatic stabilizers like transfer payments

B. The ratings agencies will then decide to downgrade U.S. Government debt which will lead to:

1. An increased budget deficit

2. Much higher interest rates

3. A massive sell off by all the major holders of U.S. Government debt, ( Many pension and insurance companies have it built into their computers to automatically sell bonds that are not AAA rated)

4. A further downgrade of U.S. debt

5. A massive sell off by China

For those of you who are still skeptical (most of you will be) read this speech by our Chairman of the Federal Reserve, it should help put some things in perspective. One thing to keep in mind is that when the Central Bank Chairman warns about fiscal sustainability it is usually a sign of too little will be done and whatever is done will be much too late in the game to make a difference.

As Ben puts it,

"The path forward contains many difficult tradeoffs and choices, but postponing those choices and failing to put the nation's finances on a sustainable long-run trajectory would ultimately do great damage to our economy."

Subscribe to:

Posts (Atom)