From Monetary Policy Actions and Long-Run Inflation Expectations by Michael T. Kiley:

"the degree of anchoring of inflation expectations is central in most empirical and theoretical applications – as inflation is a function of inflation expectations..."

It is important for us to know about future inflation so we need to gauge long-run inflation expectations. In theory firms price inflation into labor contracts and this sets the actual rate of inflation. So by looking at current long-run inflation expectations we can see what inflation will be in the future.

1) "Sticky Price" CPI :

Produced by the Atlanta Fed and research on it by the Cleveland Fed.

2) Gold and other commodities:

If you ever look at the real price of gold vs. University of Michigan's Inflation Expectations Survey you will see what I am talking about.

3) Difference between Nominal and Inflation Indexed Bonds:

The difference is expected inflation as it moves in response to news about the economy.

4) Survey of Professional Forecasters:

http://www.philadelphiafed.org/research-and-data/real-time-center/survey-of-professional-forecasters/2010/survq210.cfm

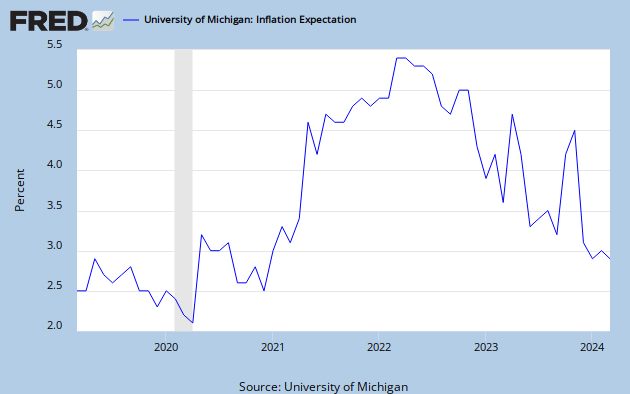

5) University of Michigan Survey of Inflation Expectations:

This shows inflation expectations for the next 12 months.

Things which impact inflation expectations include monetary policy and output. Tighter monetary policy lowers inflation expectations while looser monetary policy traditionally raises inflation expectations. Furthermore, higher levels of output raise measures of inflation expectations.

No comments:

Post a Comment