1) production and income

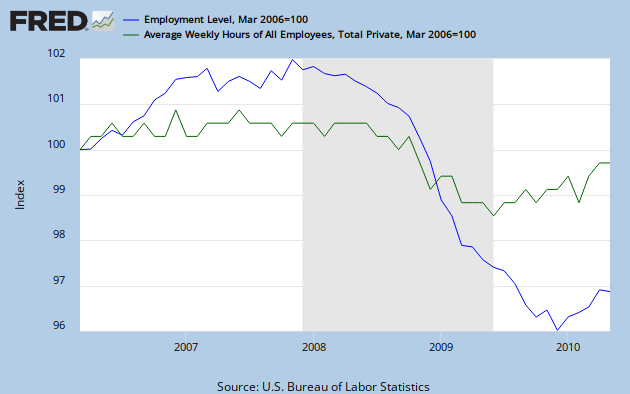

2) the job market and hours worked

3) personal consumption and housing

4) sales, inventories and orders

How does one go about interpreting the index?

A value of 0 means that the economy is growing at potential and inflation pressures are steady. Greater than > 0 and demand outstrips supply and we see inflation pressures flare up. Less than < 0 and the economy is growing below potential which can lead to rising unemployment.

The Chicago Fed National Activity Index was released today with the 3-month moving average reading 0.28. What does that mean exactly?

First of all we like to look at the CFNAI-MA3 (3-month moving average CFNAI) because it is less volatile than the month-to-month value and revisions in the data have already been incorporated. The following have been observed:

< -.7 = chance of recession has risen substantially

< -1.5 = in a recession

> 0.2 = recession likely over

> 0.7 = inflation is in danger of accelerating

A reading of 0.28 therefore implies:

0.2 < 0.28 < 0.7

Which in words means that the recession is likely over and the economy is in no danger of inflation.