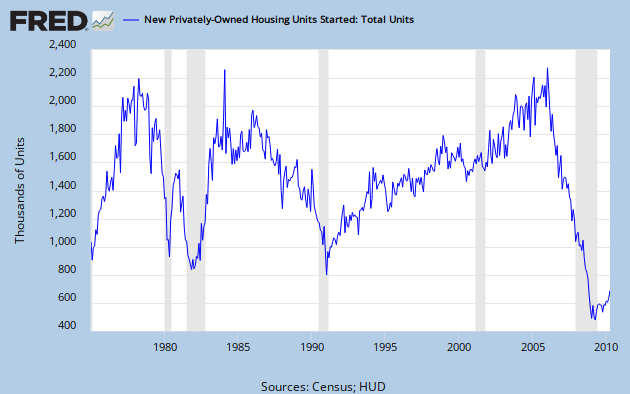

Why look at housing to gauge whether the U.S. is in a fragile state? Except for one instance, there has never been a recession at a time when the housing sector was strong. The following graph tells the tale of housing starts (you can see that in 2001 the housing market was strong and the recession was brief) and recessions:

As you can see, residential real estate is among the first sectors to shut down when the economy approaches recession and one of the earliest to take off when the economy starts to turn around. The small spike in housing starts can be explained by the home buyers tax credit which expired as of April 30th. Now the standard explanation for all this suggests that when mortgage rates fall and housing prices decline interest in home buying is rekindled now that it is more affordable. Builders in turn rush back to banks before the cost of borrowing goes up again.

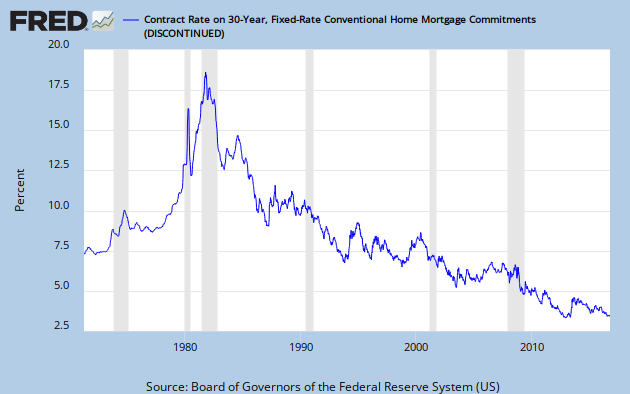

A look at the 30-year conventional mortgage suggests that rates are at an all time low:

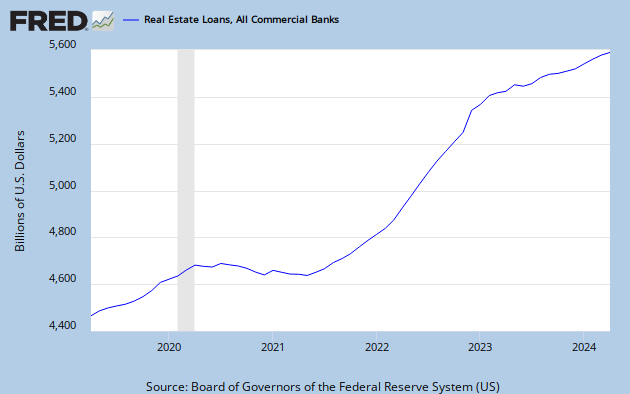

But borrowing is hard to do with commercial banks decreasing the amount of real estate loans that are

on their balance sheets (in the 2001 recession banks kept increasing the amount of real estate loans):

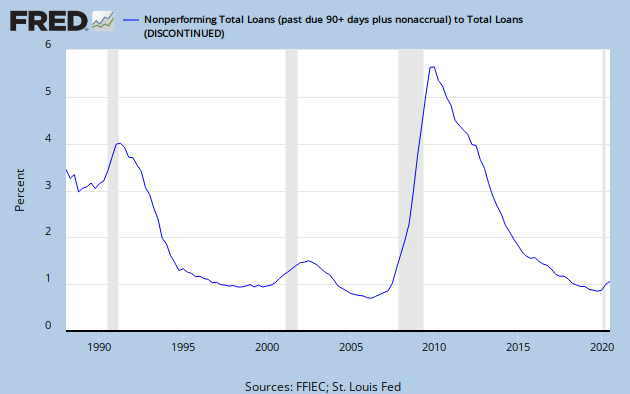

This is understandable with the ratio of nonperforming loans going up:

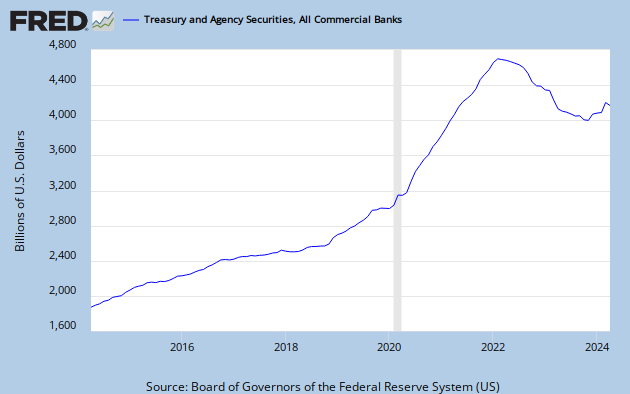

And the resulting "flight to quality" as commercial banks increase their purchase of U.S. Treasuries:

These graphs make the case for the double dip because without any demand for and supply of housing loans we are going to see a very fragile and painful recovery.

Steve I must say, I think your simple writing style makes things like this (which I consider kinda boring) a lot easier to digest. lol. Good post.

ReplyDelete