A decrease in aggregate demand leads to a reduction in some combination of wage rates, employment, and hours worked per employee. It the demand for a firms output falls substantially, a firm must either reduce its employment, average weekly hours worked or average hourly wage rate. Quit rates decline during recessions because few jobs are available at other firms. The standard New Keynesian explanation tells us that when we experience a decline in aggregate demand firms will likely lay off employees and reduce average weekly hours worked rather than resort to a reduction in wage rates. This is due to the employees strong resistance to wage cuts. On our journey we will see various things that confirm and confront this theory.

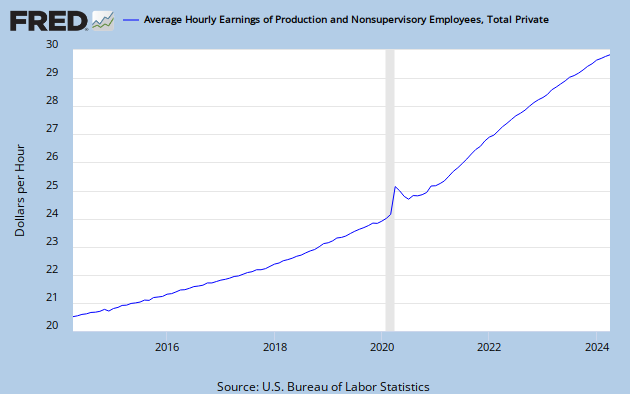

First a look at average hourly earnings:

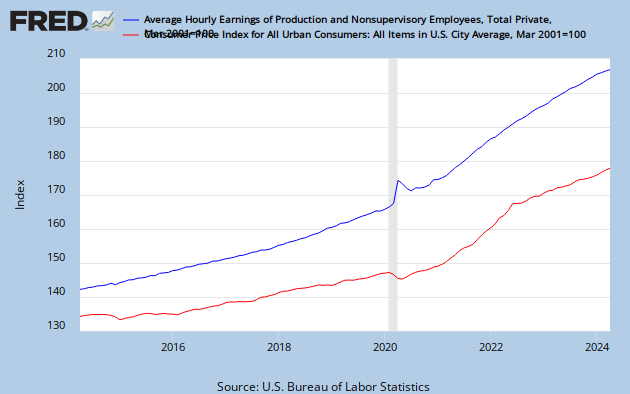

Notice how wages go up in recessions? These wage increases are remarkable given how low our inflation has been. Aren't wage increases supposed to increase inflation? To see if this relationship holds we must plot inflation and wages on the same graph. We should see average hourly wages and inflation rise at the same time:

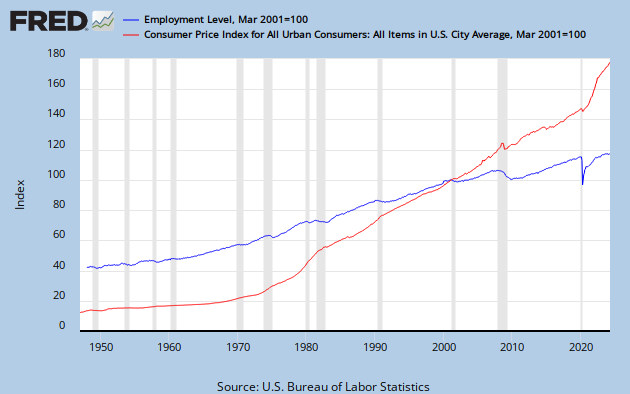

This relationship is strikingly dead on. Except we do see that recent dip in the CPI which reflects how layoffs (or a decline in civilian employment) resulted in the drop in aggregate demand:

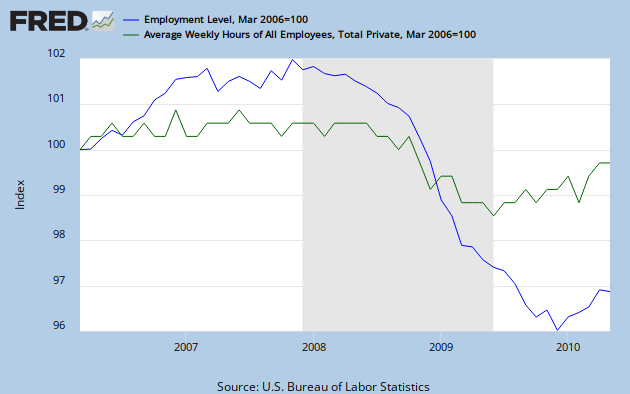

Another thing to note is average weekly hours worked. According to the theory average weekly hours worked would decrease while employment started to decrease and vice-versa:

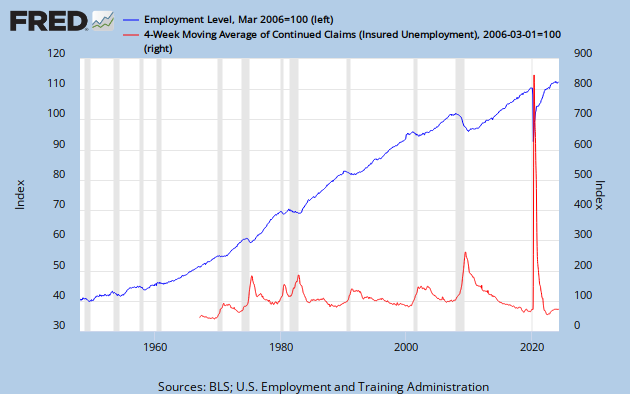

Unemployment insurance is also said to provide an incentive for firms to lay workers off rather than reducing their pay:

If reductions occurs they will most likely be in the form of layoffs and hour reduction instead of reductions in wage rates.

ReplyDelete